Today is a good time to Learn About the Electronic Trading Network and How ECN Trading can Make You Money

An Electronic Trading Network (Electronic Communications Network) ECNs are electronic trading systems which automatically match buy and sell orders at specific prices. There are other types of Networks like Electronic Grain Trading, for example. Stock Market ECNs register with the SEC as broker-dealers.

Among subscribers to ECNs are institutional investors, broker-dealers, and market-makers – can place trades directly with an ECN. Individual traders should have a brokerage account with a stock or commodities broker before their orders may be placed on an ECN for trade execution. When seeking to buy or sell securities, ECN subscribers typically use limit orders. ECNs post orders on their systems for other traders to view. The ECN will then electronically match orders for execution.

If a subscriber wants to buy a stock through an ECN, but there are no sell orders to match the buy order, the order can't be executed until a matching sell order comes in. If the order is placed through an ECN during regular trading hours, an ECN that can't find a match may send the order to another market center for execution.

Trade Execution - What Every Trader Should Know

When you place an order to buy or sell, you might not think about where or how your broker will execute the trade. But where and how your order is executed can impact the overall costs of the transaction, including the price you pay. Here's what you should know about trade execution:

Trade Executions Are Not Necessarily Instant

Many investors who trade through online brokerage accounts assume they have a direct connection to the securities or futures markets. But they don't. When you push that enter key, your order is sent over the Internet to your broker — who in turn decides which market to send it to for execution. A similar process occurs when you call your broker to place a trade.

While trade execution is usually seamless and quick, it does take time. And prices can change quickly, especially in fast-moving markets such as involving "electronic grain trading" for example. Because price quotes are only for a specific number of contracts or shares, investors may not always receive the price they saw on their screen or the price their broker quoted over the phone. By the time your order reaches the market, the price of the stock could be slightly or very different.

No SEC regulations require a trade to be executed within a set period of time. But if firms advertise their speed of execution, they must not exaggerate or fail to tell investors about the possibility of significant delays.

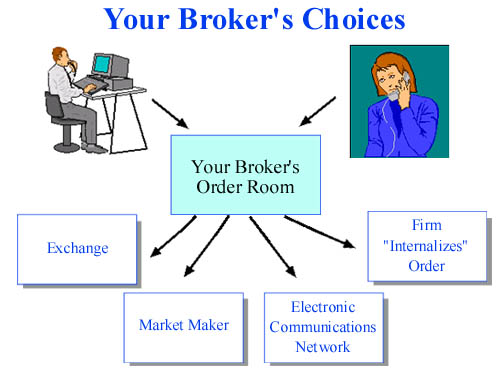

Your Broker Has Options for Executing Your Trade

Just as you have a choice of brokers, your broker generally has a choice of markets to execute your trade:

1. For a stock or futures listed on an exchange, such as the New York Stock Exchange (NYSE) or CME, your broker may direct the order to that exchange, to another exchange (such as a regional exchange), or to a firm called a "third market maker." A "third market maker" is a firm that stands ready to buy or sell a stock listed on an exchange at publicly quoted prices. As a way to attract orders from brokers, some regional exchanges or third market makers will pay your broker for routing your order to that exchange or market maker—perhaps a penny or more per share for your order. This is called "payment for order flow."

2. For a stock that trades in an over-the-counter (OTC) market, such as the Nasdaq, your broker may send the order to a "Nasdaq market maker" in the stock. Many Nasdaq market makers also pay brokers for order flow.

3. Your broker may route your order – especially a "limit order" – to an electronic communications network (ECN) that automatically matches buy and sell orders at specified prices. A "limit order" is an order to buy or sell a stock at a specific price.

4. Your broker may decide to send your order to another division of your broker's firm to be filled out of the firm's own inventory. This is called "internalization." In this way, your broker's firm may make money on the "spread" – which is the difference between the purchase price and the sale price.

Your Broker Has a Duty of “Best Execution”

Brokers use automated systems to handle trader orders they receive from their clients. In deciding how to execute orders, your broker has a duty to seek the best execution that is reasonably available for its customers' orders. That means your broker must evaluate the orders it receives from all customers in the aggregate and periodically assess which competing markets, market makers, or ECNs offer the most favorable terms of execution.

The opportunity for "price improvement" – which is the opportunity, but not the guarantee, for an order to be executed at a better price than what is currently quoted publicly – is an important factor a broker should consider in executing its customers' orders. Other factors include the speed and the likelihood of execution.

Here's an example of how price improvement can work: Let's say you enter a market order to sell 500 shares of a stock. The current quote is $20. Your broker may be able to send your order to a market or a market maker where your order would have the possibility of getting a price better than $20. If your order is executed at $20.05, you would receive $10,025.00 for the sale of your stock – $25.00 more than if your broker had only been able to get the current quote for you.

Of course, the additional time it takes some markets to execute orders may result in your getting a worse price than the current quote – especially in a fast-moving market. So, your broker is required to consider whether there is a trade-off between providing its customers' orders with the possibility – but not the guarantee – of better prices and the extra time it may take to do so.

You Have Options for Directing Trades

If for any reason you want to direct your trade to a particular exchange, market maker, or ECN, you may be able to call your broker and ask him or her to do this. But some brokers may charge for that service. Some brokers offer active traders the ability to direct orders in Nasdaq stocks to the market maker or ECN of their choice.

SEC rules aimed at improving public disclosure of order execution and routing practices require all market centers that trade national market system securities to make monthly, electronic disclosures of basic information concerning their quality of executions on a stock-by-stock basis, including how market orders of various sizes are executed relative to the public quotes. These reports must also disclose information about effective spreads – the spreads actually paid by investors whose orders are routed to a particular market center. In addition, market centers must disclose the extent to which they provide executions at prices better than the public quotes to investors using limit orders.

These rules also require brokers that route trading orders on behalf of customers to disclose, on a quarterly basis, the identity of the market centers to which they route a significant percentage of their orders. In addition, brokers must respond to the requests of customers interested in learning where their individual orders were routed for execution during the previous six months.

With this information readily available, you can learn where and how your firm executes its customers' orders and what steps it takes to assure best execution. Ask your broker about the firm's policies on payment for order flow, internalization, or other routing practices – or look for that information in your new account agreement. You can also write to your broker to find out the nature and source of any payment for order flow it may have received for a particular order.

If you're comparing brokerage firms, ask each brokerage firm how often it gets price improvement on customers' orders. And then consider that information in deciding which brokerage firm you will do business with.

Recommended Trader Resources

![]() The trading and day-trading Knowledge Source website Traders Organization

The trading and day-trading Knowledge Source website Traders Organization